A Brief - Roxy Pacific (RPH) is a small-mid scale Singapore property developer with some investments in commercial property, mainly in the East Coast, District 15 area.

Why this counter is a buy

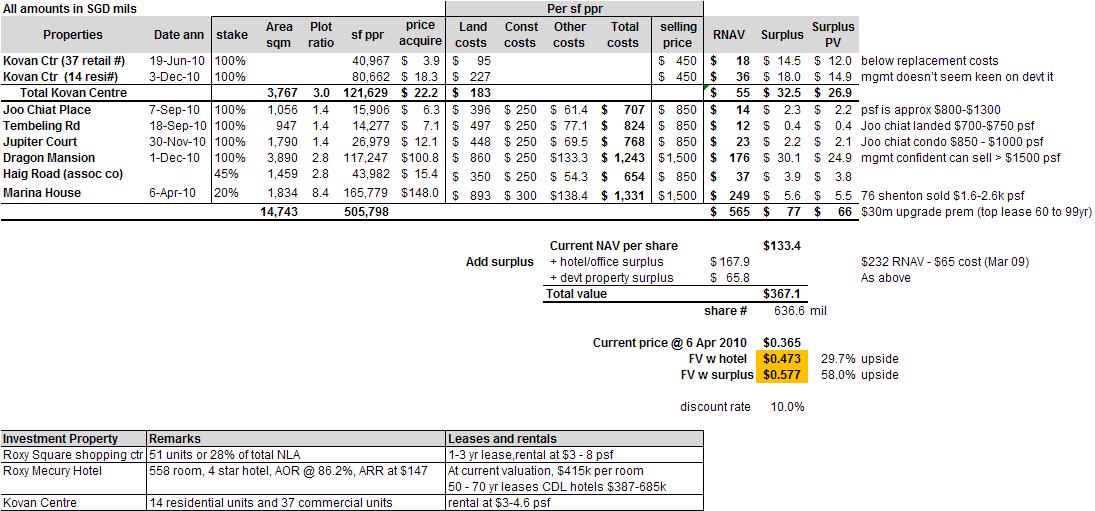

- Substantial discount to RNAV (the freehold hotel value is carried at cost).

- Astute management (cheap acquisitions in the areas, all below S$ 500 psf ppr)

- Long experience in the district 15 (Founder's father used to operate in that region

- Blockbuster year for 2010/2011 as S$280m worth of revenue unrecognized and with approx 15-17% net margins equate to S$42-47m worth of value

- Trading at steepest RNAV discount to peers - Sim Lian, Heeton, Sing Hldgs and Soilbuild

- Firm enjoys a 6 year long history of high growth, ROE 20% and net margins over 20%

Risks (Killing my own idea)

- Firm is very selective in acquisitions and may run out of land bank

- Currently 6 projects will last them approximately 2 years, streak ends there

- Hotel stocks typically trade at 40-50% discount to RNAV (But historically also plagued with other issues, for example Orchard Parade has money losing yeo Hiap Seng etc)

- Overall market dip (financial + property)

Expectations

- Deep discount versus other small hotel owners cum property developers is illogical given the strong management, high quality freehold hotel as well as a record of 100% sales for their developments within a short period of time

- Did up a simple RNAV, took psf prices of Joo Chiat properties at S$850psf which is a very conservative estimates. Lately the area has been going for over S$1000 psf for 99 year leasehold small developments

- Even if assuming the developments are worth zilch, 0.8x price to NAV with only the revalued hotel will give a value of S$0.378 and 1x gives S$0.473.

- Downside is little since most of their developments sell out, hotels are seeing improving vacancies and even if that fails, the land under it is valuable since it stands opposite Parkway Parade, Marina area where even HDBs are going for S$800,000 for a 5 room flat

- Downside support price will be S$0.378 or higher, upside will take care of itself

{kind=link}

1 comments:

Cannot take away anything from that stock.

Post a Comment