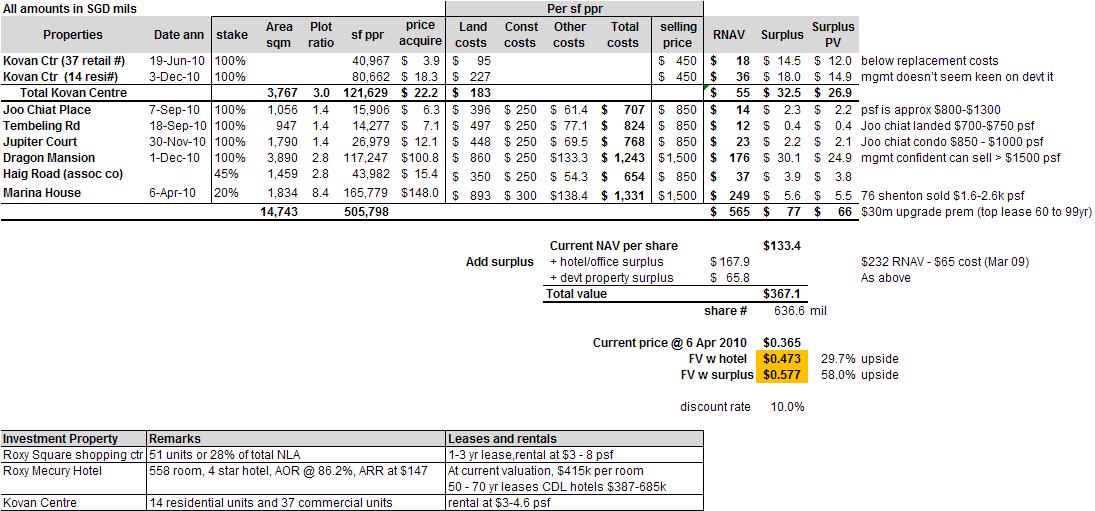

I do not pride myself as a macro guy but this data is pretty insightful, it took me a while to get the table done but was well worth the effort. I will not be liable for any reliance on the information to make investment/s. decisions.

Click HERE if you are new to ratings, very good explanation by Blaha Finance.

- Greece

- S&P downgrades from AA to BB-

- Total debt of Eur 305 bn vs 2009 GDP of Eur 237 bn

- If it takes Eur 45 bn (30 EU and 10 IMF) repayable on 2013, adding on to existing Eur 34 bn of interest and principal, thats approx Eur 74 bn or 31% of Greece's GDP

- Do not forget that each year, Greece ha to pay approx 10-15% of its GDP to pay off existing debts till at least 2017 where the debt payment slows to 5-10%

- Comes back to the point in my 1st post that a troubled country like Greece should not have sovereign yields for its debt. Previous news on traders scalping yield for 10 year Greek debt of 7+% to 6.5% was out of this world. True enough, now its over 10+%, 2 year at 15%. Well, you do not need a rating agency to tell you that Greek debt is junk status. It will and should stay at these yields or higher.

- Portugal

- S&P cuts rating from A+ to A-

- Spain's largest trading partner

- Face a slow growth issue with wages rising faster than productivity

- Plans to have a 50% tax on "highly paid" finance executives

- Spain

- Debt to GDP much lower than Greece

- Real estate bubble boom pulled in jobs and now the bust is killing it

- Country has product manufacturing quality issues and unable to adjust wages

- Inefficient taxation system especially for property trades piles on the problem

- Debt wise not as leveraged as Ireland or Greece

- Slow growth and void from real estate will hamper recovery

- Look at charts below, July 2010 is a lumpy debt payup for Spain

- UK

- Commercial lending grows 5-10% yoy from 1999 to 2007 is actually declining in 2010

- Debt level remains high

I highlighted in bold potential debt default candidates. Reading news and all do not give a clear view of the amount of risks lies therein the sovereign debt until you assemble the numbers. The European countries in bold look awfully bad especially Ireland. Now US does not seem so bad relatively aint it?. Theres always a price to pay for something.

Click on the picture above to enlarge and see the otherwise invisible GDP growth yoy.

Now the main bulk of the problem is Euro nations hold the debt of each and other. So if one falters, there is a strong incentive or rather disincentive to all rush and support that nation. So increasingly we can see the stress lines from Greece and now from Portugal and now likely Spain.

Now the main bulk of the problem is Euro nations hold the debt of each and other. So if one falters, there is a strong incentive or rather disincentive to all rush and support that nation. So increasingly we can see the stress lines from Greece and now from Portugal and now likely Spain.

Foreign banks are holding alot of Greece and Portugal debt and less of Spain. However Euro banks are holding alot more Spain and Ireland debt. However, countries in immediate distress are those with high government debt to GDP and with poor GDP growth figures, not total debt to GDP. Spain is in trouble as it has over Eur 225 bn worth of debt due in 2010 (lumpy debt maturity), equivalent to Greece's economy. Adding to the problem, Spain has the highest budget and current account deficit in the world second to Iceland. However, noting its low debt relative to other troubled nations, its problem will be a slow one to come up and a likely economic recovery may save it from a fate like Greece.

Source: Bloomberg

Foreign banks are holding alot of Greece and Portugal debt and less of Spain. However Euro banks are holding alot more Spain and Ireland debt. However, countries in immediate distress are those with high government debt to GDP and with poor GDP growth figures, not total debt to GDP. Spain is in trouble as it has over Eur 225 bn worth of debt due in 2010 (lumpy debt maturity), equivalent to Greece's economy. Adding to the problem, Spain has the highest budget and current account deficit in the world second to Iceland. However, noting its low debt relative to other troubled nations, its problem will be a slow one to come up and a likely economic recovery may save it from a fate like Greece.

On the other hand looking at reserves

I think it may be wise to

- Long Singapore dollar and Russian Ruble

- Short the US dollar, Euro and the Pound

- If you are in the market

- Sell losers into strength, winners up to you

- Stick with only the best names

- OR if you are like me,stay >50% cash

With the risk aversion and likelihood of cross default among Euro nations, we see a across the board decline in the stock indices. Please also note short US and/or Euro is a long term view. In the short term, both may rise in view of the falling markets due to unwinding from risk aversion trades. Do not ignore this development as US / Eur has one of the largest money supply around and unwinding may prove to be painful to those who short the USD or Eur early.

{kind=link}